By Reed Shapiro

In February of 2019, my colleague, Pianpian Wang, penned an article that discussed how carbon gets priced around the world, in both the compliance and voluntary carbon markets. Pianpian’s article focuses on the origins of price dynamics in both compliance trading systems, and voluntary measures. Just a year and a half later, however, much has changed. This post serves as an update to Pianpian’s first article and a practical guide on what to expect when looking to purchase carbon offsets.

According to the World Bank’s Carbon Pricing Dashboard, which tracks all jurisdictions with carbon pricing initiatives or policies, like carbon taxes by the metric tonne, or cap-and-trade systems in which entities emitting over a certain threshold will be economically penalized by having to purchase excess cap space at a premium, the number of initiatives jumped from around 50 from the time of Pianpian’s article, to 61 today. With the projected launch of China’s national emissions trading system (ETS), by 2021 World Bank estimates the compliance markets will collectively ‘cover’ 12 billion metric tonnes of Carbon Dioxide equivalent (12 Gt CO2e), or 22.3% of the a total estimated 53 billion metric tonnes of greenhouse gas emissions.

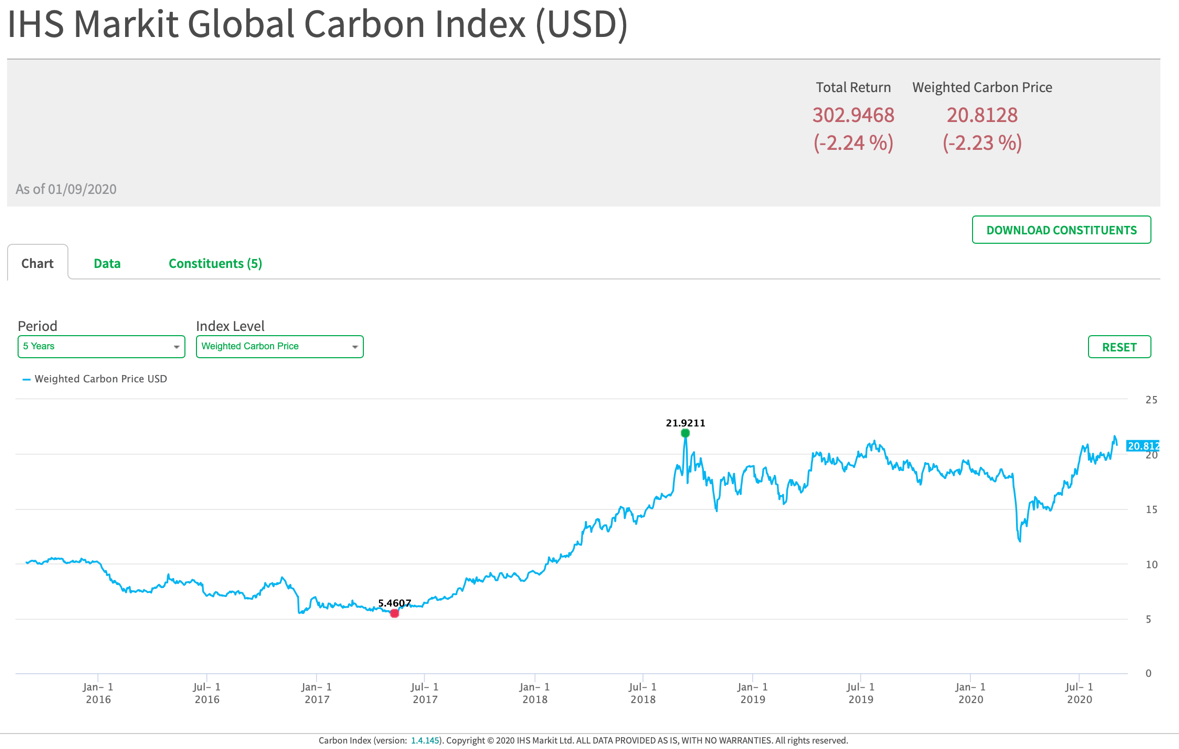

The pricing of the EU ETS, which dropped from its height of EUR 24,5 in 2019 (Financial Times has the highest mark at EUR 29,27 in July of last year), to EUR 18,53 in 2020, has turned out to be a fairly good indication of the rest of the worlds’ mandatory carbon markets performance. According to IHS Markit’s Global Carbon Index, which is made up of prices from the California Compliance Allowance, RGGI, and European Allowance prices, the current weighted global price on carbon is equivalent to $20.81 USD (shown in the chart below). The World Bank’s data comes out with a similar price across its 61 jurisdictions at $20.11 per tonne.

Given that the California cap-and-trade system has now linked with Quebec’s, and that even though there is no recent news regarding California’s potential merge with China’s ETS, people have been studying the EU ETS and California system in an effort to apply the best learnings from these systems into the Chinese ETS. There is mounting evidence that the once fractured global price on carbon in the compliance markets is indeed coalescing into a universal price on carbon—that is at least when it comes to allowances.

As Pianpian mentioned in her previous post, the capacity for these systems to all link in a truly unified, universally instituted price on carbon ultimately depends on our collective capacity to work it out on a rules and regulations level. A price on carbon is only as high or low as the rules that institute it in the first place allow it to be via manipulation or market forces.

Shift, now, to the voluntary carbon markets, or the remaining 41 billion metric tonnes of CO2e which industries, companies, and non-governmental bodies are working to reduce to net zero by mid-century. While the voluntary carbon markets are seeing major increases in trading volume, a universal price isn’t yet apparent.

While in Pianpian’s 2019 post the market benchmark held steady around $3—$6 USD, upon looking at Gold Standard Foundation’s ‘marketplace’ one will see there isn’t a project featured for less than $10 USD. Most projects listed in the marketplace are priced at $15, $18 and $20; one even fetches $47. Beyond these benchmarks, I personally have seen more and more price-points directly from project developers validated by the Climate Action Reserve, Verra, and American Carbon Registry that are north of $10.

Furthermore, where buyers were quibbling over whether they could get their costs per tonne down to $5 just a few years ago, as Pianpian mentioned 18 months ago, the private sector has indeed rushed towards more involvement in the voluntary markets. Preference has gravitated more so towards quality, socio-economic co-benefits, and project-type and location specifications.

Each of these individual qualifying attributes (standard, project type, project size, location, community involvement, other co-benefits) plays a part in increasing the settling price in the market, and often corporate buyers, eager to show they’re best-in-class, spare no expense.

It seem that projects priced below $3 are still available, and there is no shortage of voluntary buyers looking for the cheapest credits they can get their hands on. Ecosystem Marketplace mentions that buyers do desire projects with $10 co-benefits, but they ‘balk’ at paying top dollar. These days of choice by price, however, are likely waning. As more large companies make large voluntary commitments, and as old projects are phased out in favor of those more integrated, more technologically advanced project types, volumes of available supply will diminish, and even Ecosystem Marketplace may end up reporting prices that more closely track those referenced on Gold Standards’ platform.

There is still something for everyone in the voluntary carbon markets, yet as corporate, state, and national climate commitments to reducing emissions continue to pick up momentum (both in size of the commitment, and volume of committed entities), we may quickly transition from a buyer’s market to one in which supply is drastically reduced when compared to the rate at which new market participants are looking to offset their emissions.